Initiating Coverage [ACTIONABLE IDEA #1]: A Capital-Light Microcap Trading At A 50% Discount to Peers

An undiscovered Polish microcap with high growth, high ROIC, an impenetrable moat, and best of all, a low valuation.

In this newsletter, I intend to cover immediately actionable ideas as I find them. These ideas may include a special situation or simply a stock that is currently undiscovered and trading at a low valuation. The latter is the case now for Immediately Actionable Idea #1. These ideas and their performance will be tracked over time.

Conviction level: Medium

Risk level: Medium-High

Immediately Actionable Idea #1 has the following characteristics:

IAI #1 is a Polish microcap trading on the Warsaw exchange with a market cap under $100M USD.

The average trading volume is approximately $100k USD per day, making it suitable for only individual investors and small funds.

I have not seen this idea posted or discussed anywhere else in detail. There are only a handful of posts on X/Twitter ever covering the company, and I believe this write-up is the first ever English write-up on this company.

The company sells a product that cannot be directly disrupted or replicated due to the nature of the product having limited physical availability, granting this company a strong moat.

From 2021 to 2023, the company doubled revenue and tripled gross profit. Net profit increased 2.5-fold.

This company is capital light and has global industry-leading margins.

The company trades at under 7X 2024 EBITDA, under 10X 2024 EPS, and under 10X 2025 estimated EPS. Multiples that, given its quality and growth rates, I believe may ultimately prove far too low.

Peers trade at average multiples closer to 10X NTM EBITDA and 15 NTM P/E, putting this company at around a 50% discount to peer averages.

Given the company’s growth rates and low starting valuation, I believe there is little multiple compression risk, but moderate to high short-term earnings risk in the event of a recession.

This company has earned an ROC of 35% and an ROE of 42% over the LTM.

Let’s dive in!

Immediately Actionable Idea #1 is Digital Network SA. It trades on the Warsaw exchange under the symbol DIG (or DIG.WA if including the exchange in the ticker). The only way to buy it is to have access to the Warsaw exchange. I use Interactive Brokers to achieve this, and for my Canadian readers, I am not aware of any other broker that has access to the Polish markets.

Digital Network is Poland’s leader in the Digital Out-Of-Home (“DOOH”) advertising market. The DOOH market simply means selling advertising space on digital screens in public spaces. They compete against other DOOH companies, as well as traditional Out-Of-Home (“OOH”) advertising companies that use non-digital advertising placements on things like billboards and bus stops. Many companies operate in both DOOH and traditional OOH, but the market is moving further toward DOOH companies over time. This is due to many advantages such as dynamic pricing, flashier and more effective ads, and the ability to play videos as opposed to a static printed image.

Digital Network is positioned as the leader in this growing DOOH market in Poland.

Business History

Digital Network only reports in Polish, and information on the company is limited. Simply searching Google and AI tools won’t get you far with this company. Even Digital Network’s own reports are sparse.

Fortunately, the Warsaw Stock Exchange launched an Analytical Coverage Support Program1 in 2023 to have exchange-sponsored research reports produced on companies like Digital Network. These are meant to be neutral reports, though they’re likely biased bullish. Nonetheless, the information in these reports for Digital Network is by far the most useful source I’ve found. These reports are in Polish, but I’ve used a translator to convert the most recent one to English, and made the translated version available at the bottom of this article.

In 2003, Dariusz Stokowski founded a company he called 4fun.tv Sp. z.o.o. that owned and operated it’s own Polish television channel. This channel ran music and entertainment shows aimed at the 16-49 age demographic. The company IPOd on the Warsaw Stock Exchange in 2010 as 4fun Media. In 2014, the company then invested in a website known as naekranie.pl. that provides digital content for online distribution.

In 2015, 4fun Media would make its most important investment. 4fun Media acquired a majority stake in the Digital-Out-Of-Home (DOOH) advertising company ‘Screen Network.’ They also acquired the advertising agency ‘Bridge2Fun.’

The company continued to make investments and acquisitions in 2018, acquiring several e-commerce websites focused on lifestyle fashion, such as Mustache.pl and PingBig.com. It appears these are now mostly defunct.

Consistent with the typical microcap company, nearly all of these investments proved unsuccessful. In 2019, management initiated a recovery plan. By 2020, 4fun Media had sold off its television channel, some of its advertising agencies, the digital content platforms and websites, and either shut down or sold all of the e-commerce operations, leaving it with just the DOOH segment.

In 2022, the company changed its name to Digital Network SA. It has since focused on growing and expanding its DOOH network.

Business Model/Revenue Generation

Digital Network sells advertising on large-format LED and LCD screens in highly trafficked public locations. These screens are placed in strategically in both indoor locations (think inside high-traffic facilities such as airports, train stations, or malls) and outdoor locations (placed on the outside of buildings on popular streets, bus stops, etc.). These may also be placed in locations that replace traditional billboards. The outdoor segment accounts for about 70% of the market, while the remaining 30% of the market is indoor.

The DOOH advertising market generally prices advertising on a time-allotted basis with dynamic pricing for peak times. In the traditional OOH market, companies ‘rent’ space on surfaces such as billboards or bus stops, usually for a set amount of time. Digital has the advantage of being more dynamic, as the advertisements can change or rotate at any time. This allows DOOH companies to sell slots in the rotation, or price based on time and impressions, with real-time updates.

Both OOH and DOOH sell ads through direct sales, their own advertising agencies, or through third-party advertising agencies. My understanding is that Digital Network does all of the above. One development in the way ads are sold due to digital has been the development of a programmatic sales channel, which simply means unfilled ad slots are auctioned off in real time. As digital takes share from traditional, I would expect further innovations to occur.

Total Addressable Market

The global DOOH advertising market is a $20.7B USD market and is expected to grow at 10.7% until 2030 when it’ll be a $34B+ market. Some estimates have the market growing significantly more than this.

The European DOOH market as of 2024 is estimated at $5B and is expected to grow at 11% to $9.9B by 2030.

The total OOH market (which includes DOOH) in Poland as of 2023 was about 650M PLN, or $170M USD. Of that, approximately one-quarter of it was digital, or about 160M PLN. That figure has grown from just 11% of the total in 2019 to 25% in 2023.

Digital Network did 65M PLN of revenue in 2023, giving them about 40% market share of the DOOH market and 10% market share of the total OOH market.

Competitive Analysis and Industry Position

Competitive Environment

Firms in this industry compete in a few ways. First, they compete for the right to locations. These locations are often rented from property owners. Once leases expire, they must compete again to secure locations. When screens are placed on buildings, it’s usually the building owner that dictates terms, while things like bus stops/shelters or even the exterior of buses themselves are dictated by city contracts that firms bid for.

Second, firms compete on differentiation. More premium locations mean more impressions and higher ad pricing. Further differentiation can come from the types of screens used, such as 3-dimensional anamorphic screens2.

Finally, firms compete on price. Given that there is some differentiation, price is not always the most important consideration, but it is often a factor.

Competitors

Agora SA

Agora SA is the largest OOH company in Poland and is listed on the Warsaw stock exchange under the symbol ‘AGO’. It has a 486M PLN ($126M USD) market cap and a 1.2B PLN enterprise value due to its extensive 686M PLN of debt.

Agora is a conglomerate3 that engages in five segments: Movies and books, digital and printed press, outdoor (OOH), internet, and radio. This analysis will focus on its OOH segment.

Within Agora’s OOH segment, Agora operates through its subsidiary AMS (Art Market Syndicate). AMS has roughly a 30% market share in the overall Polish OOH market with a focus on municipal contracts for bus shelters and citylights (my understanding is that citylights are essentially static LED lit posters). AMS is concentrated in the traditional OOH market. As a consequence, they’ve recently seen OOH segment revenues decline as advertisers shift towards digital solutions.

AMS faces challenges due to their fragmented conglomerate business constricting resources, the relatively low amount of revenue generated by the OOH segment (about 6% of total revenue), and their considerable debt burden resulting in cash flow going toward paying off debt, rather than being able to invest in DOOH.

Agora is a company that investors in Digital Network need to pay attention to. They’re credible, but are unlikely to threaten Digital Network for now.

Ströer SE & Co

Ströer is a OOH/DOOH company trading on the German Xetra exchange under the symbol ‘SAX’. Ströer has a €3B market cap and a €4.5B EV. The company has OOH/DOOH operations in Germany, Poland, Spain, the Netherlands, Belgrium, and the UK. They are the largest of Digital Network’s competitors.

Ströer is second only to Digital Network in Poland, operating around 10,000 digital screens in Poland with exclusive rights in the Warsaw Metro. Ströer has another 15k traditional OOH ad spaces.

Ströer is the most formidable competitor to Digital Network. They have a larger global scale and more resources. Ströer did €2.05B of revenue in 2024, absolutely dwarfing Digital Network’s €18M of revenue (converted from PLN). Ströer has 58% market share of the German traditional OOH market and they claim to have around 30% of the OOH market in Poland4.

Clear Channel Outdoor/Clear Channel Poland

Clear Channel Outdoor is a US-based OOH/DOOH company listed on the NYSE under the symbol ‘CCO’. They operated a Polish division, but as of March 31, 2025, they sold their Europe-North segment, including Poland to Bauer Media Group for $625M5. Bauer Media Group is currently a private company. We’ll have to watch and see where Bauer takes this company going forward.

Other Competitors

There are several other competitors worth considering. Cityboard Media (owned by Braughman Group) operates large-format billboards and is the leader in OOH billboards in Poland. Jet Line is another Polish billboard company that has recently moved more into digital. Synergic is a smaller competitor known for its advertising spaces in malls and bus interiors. ISM SA (publicly traded on the Warsaw exchange under the ticker IMS) specializes in sensory marketing, which includes things like smells and sounds inside malls, stores, and kiosks.

Overall, the OOH advertising market structure in Poland has been mostly captured by the largest few players. This makes it close to an oligopolistic structure.

Competitive Advantages and MOAT

Digital Network’s competitive advantages come from scale and securing high-traffic locations. Early on, Digital Network aggressively installed digital screens rather than traditional ones, allowing them to reach scale ahead of slower-moving traditional competition.

This scale now allows Digital Network to not only be insulated from new competitors (due to having locations already secured) but also allows for scale advantages involving things like spreading content and technology costs over the largest number of screens, as well as an ability to offer packages across regions that competitors cannot match.

This virtuous cycle then allows Digital Network to invest in more screens further increasing their competitive advantages.

Financials & Valuation

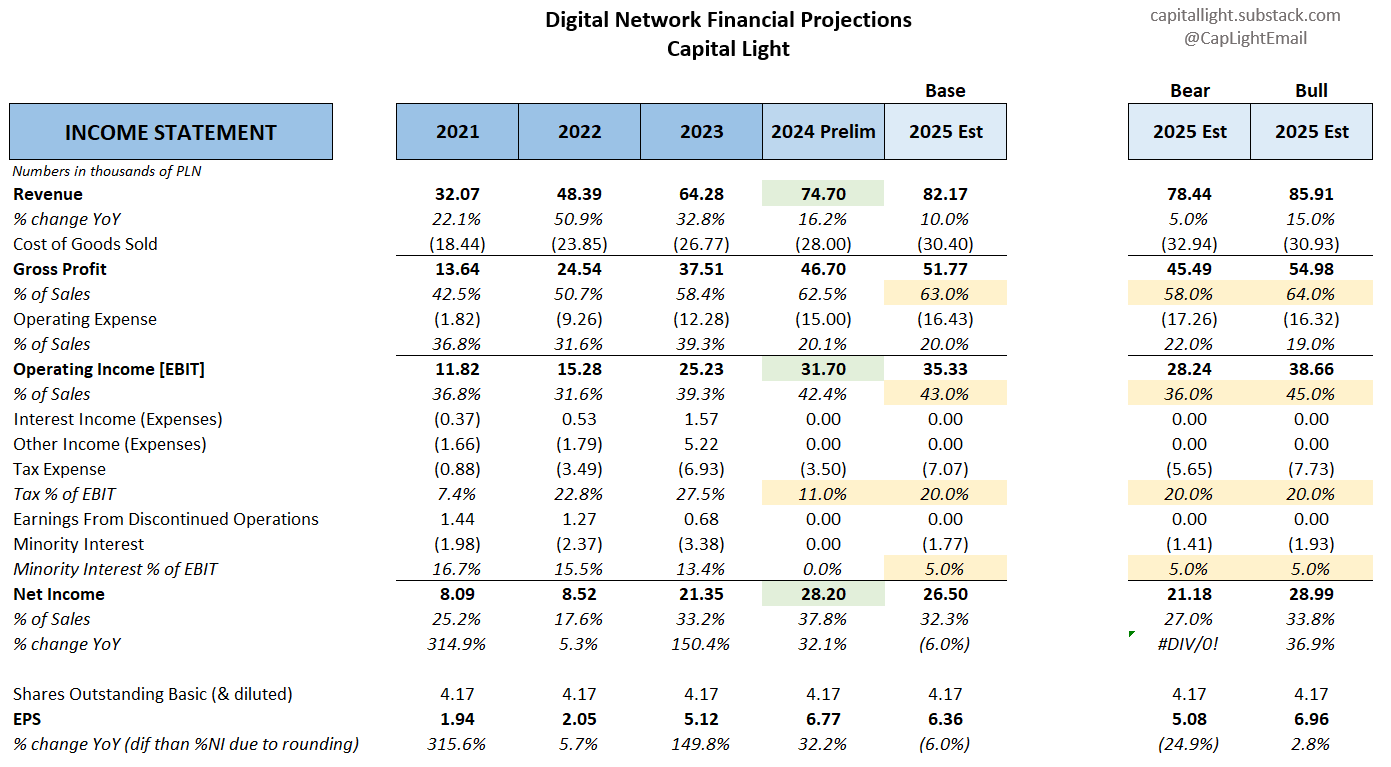

Note: The following uses historical MorningStar data sourced from TIKR.com. This appears to differ slightly from TIKR.com’s data sourced from CapIQ. Obviously, this is a problem for financial statement analysis. This appears to be a particular problem for calculations like EBITDA pre-2023. Thus, I’ve only included the income statement using MorningStar data for now, and I’ll only be discussing metrics like EBITDA based on what the company has put out for 2024 or what I estimate going forward.

Digital Network has grown revenue from $32M in 2021 to nearly $75M in 2024 (based on preliminary numbers6). This is a CAGR of 24% over four years. EPS in 2021 was 1.94 and has grown to an estimated 6.77 in 2024 (based on preliminary net income) for a four-year CAGR of 37%. These are clearly impressive numbers, but as always, the key for investors today is what growth rates will be going forward. Digital Network, in its reports, has suggested it expects to continue growing at a minimum of 10% per year. Thus, 10% revenue growth in 2025 is my base case, while 5% revenue growth is my bear case, and 15% is my bull case (see bear and bull cases in the far right columns).

Note that we only have 2024 preliminary numbers for Revenue, EBIT, EBITDA, and Net Income. This requires some filling in the blanks on cost items, which is what I’ve attempted to do here. Above the EBIT line is straight forward, but the difference between preliminary EBIT and preliminary NI is only 3.5M PLN. I’ve slotted this in tax expense for now, which makes the tax rate look low. In reality, I think there must be some sort of non-operating gain or income skewing the numbers a bit. Regardless, we won’t know until we get the full 2024 financial statements.

My base case for 2025 has the company doing 82M PLN of revenue with 63% gross margins, 43% operating margins for 35M of EBIT, a tax rate of 20%, and a minority interest portion of 5%, resulting in a final NI of 26.5M and EPS of 6.36 per share. This means my estimated EBIT is higher in 2025 than 2024, but EPS is lower. Again, EPS in 2024 appears boosted from something that we don’t know about yet. I believe my 2025 number is more representative of what normalized EPS should be going forward. My bear case has lower margins ultimately resulting in 5.08 of EPS, while my bull case has higher margins resulting in 6.96 PLN of EPS.

The stock trades at 60.90 PLN as of the time of writing, which puts the multiple of 2025’s EPS at 9.6X.

If we use EV/EBIT (which makes for a better comparison to peers due to considerably different capital structures), then Digital Network’s EV is about 262.5M7 (vs a 252M market cap). This puts my estimated EV/2025 EBIT at a multiple of 7.4.

These are not demanding multiples by any stretch. There is little multiple compression risk here. But, I do think earnings are exposed to advertising spend and thus are cyclical in nature. Should companies cut advertising expenditure in a recession, Digital Network’s stock price may fall in line with the decline in earnings.

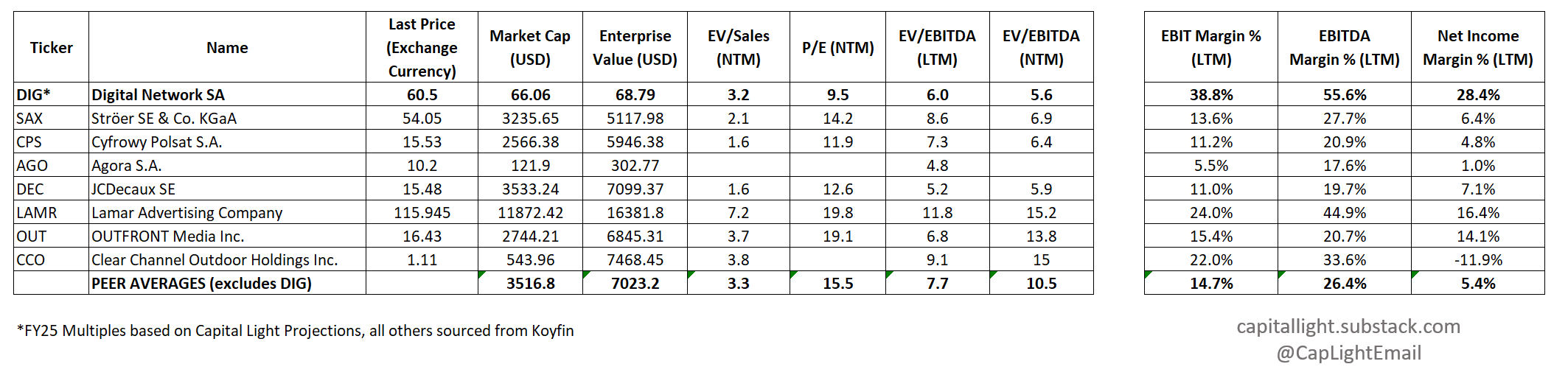

Comparing to peers illustrates that Digital Network trades at essentially half the multiple of peers on a going-forward basis and still well below average on an LTM basis, despite having industry-leading margins (see the far right three columns).

A 15 NTM P/E (peer average) on DIG would put the stock at 95 PLN, or just under 60% higher. A NTM EV/EBITDA multiple of 10.5 (peer average) would put the stock near 120 PLN, or nearly 100% higher. A NTM EV/EBITDA multiple of 7.7 would put the stock near 77 PLN, or 28% higher. Interestingly, the stock does trade at the peer average NTM sales multiple. This perhaps suggests the market thinks margins are not sustainable. However, I struggle to see how that would be the case, given this is not a company benefitting from some sort of temporary excess demand. They’re just run more efficiently than competitors.

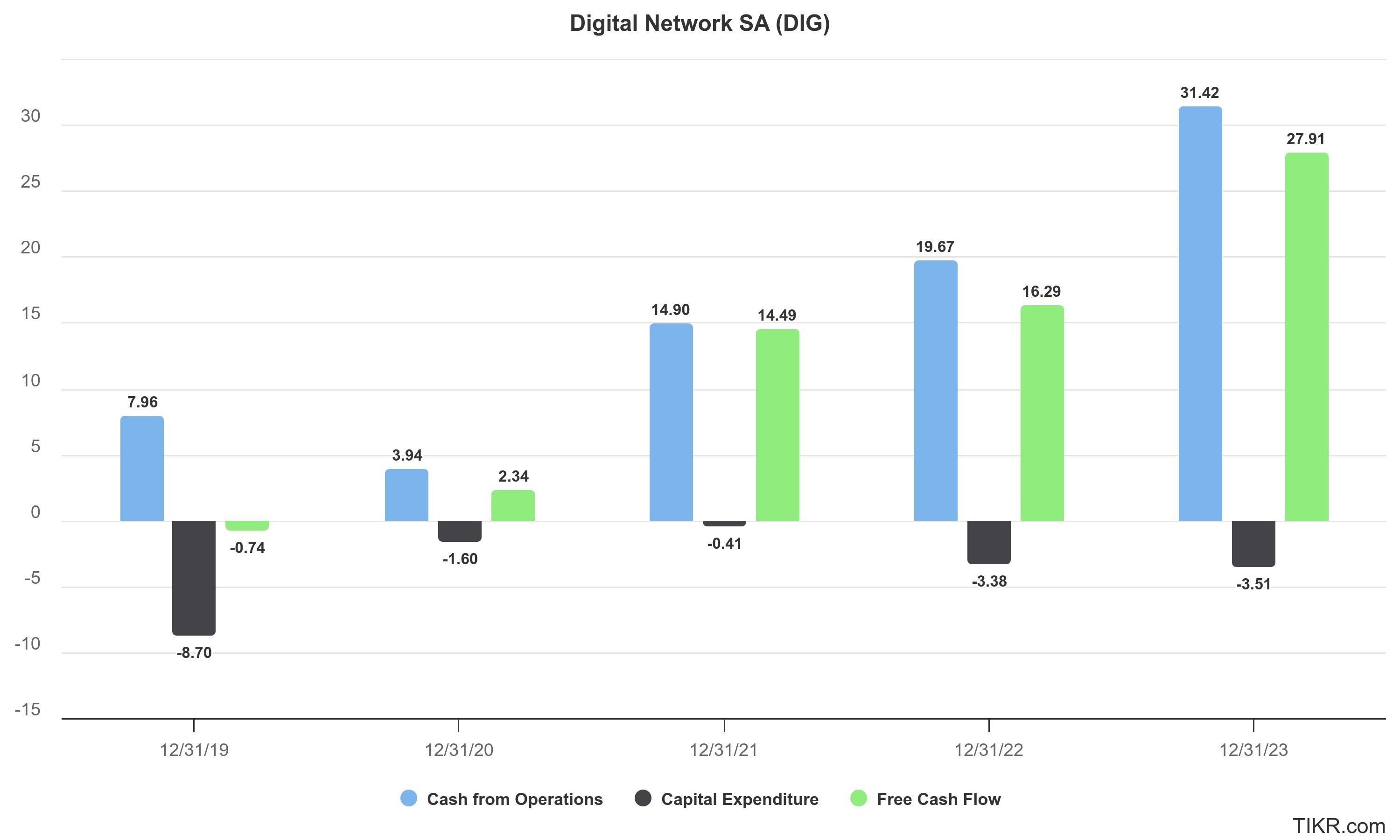

Free Cash Flow & Returns on Capital

Digital Network generates significant FCF (defined as OCF less CAPEX). The screens they buy cost surprisingly little and are just about their only form of CAPEX. The company spent a considerable amount on screens in 2019 to get going. These screens last about 10 years, so at some point, there may be a larger capital reinvestment necessary, but the company is leveraging screens already purchased to grow for now.

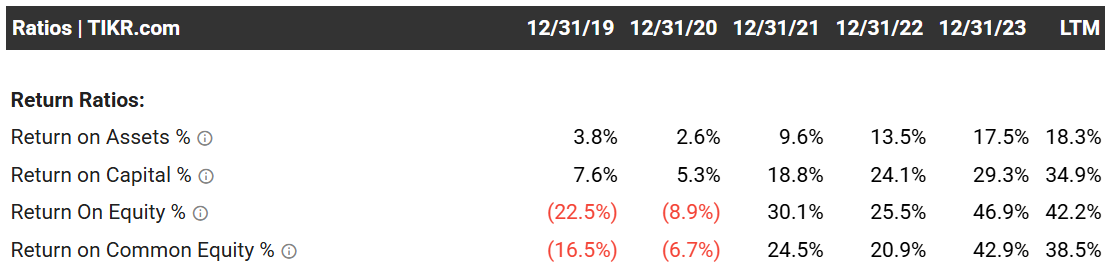

Digital Network’s returns on capital have improved considerably since divesting their old businesses and focusing purely on the DOOH market. These figures will be even better in 2024. TIKR’s ROC isn’t quite synonymous with how I usually calculate ROIC, but it’s close enough that this is easily a 25% ROIC business with room to continue investing at high rates of returns or return excess capital to shareholders, since they don’t even require much capital to grow.

Risks

The main risks for Digital Network are the following:

The obvious risk is a decline in advertising spending in a recession. This would have the potential to significantly harm the earnings, at least in the short term, of Digital Network and other players in the OOH/DOOH space.

A considerable but unlikely direct risk to Digital Network would arise if larger competitors such as Ströer began to act irrationally and used an aggressive strategy to secure locations at a loss in order to gain market share quickly.

There is technological execution risk here in both software and hardware:

This would include hardware failing and Digital Network failing to fix broken hardware in a reasonable amount of time. Advertisers may move to more reliable providers in this case.

Competitors may develop software that better delivers targeted ads, making their screens more effective.

Competitors may develop better back-end software systems to manage ads and ad inventory, fill unsold ad slots, and more.

Conclusion

Digital Network is a high quality, capital light, free cash flow generating business leading it’s niche. The stock trades for well under peer multiple averages, and is not high on an absolute basis either. This is the exact type of company I want to cover on this newsletter.

I’m experimenting a bit with the format of this newsletter, but readers can expect the next piece to come out during the week of April 13-19, where we’ll be covering a high quality, capital light French microcap company trading at under 4X earnings adjusted for their large cash balance.

Thumbnail image: Tânia Mousinho

Excel Files:

Research Reports Used:

GPW Fourth Edition of Analytical Coverage Support Programme to Launch in July: https://www.gpw.pl/news?cmn_id=114008&utm_source=chatgpt.com&title=Fourth+Edition+of+Analytical+Coverage+Support+Programme++to+Launch+in+July

Agora SA Financial Reports: https://www.agora.pl/en/reports-1

Ströer 2024 Media Kit

Digital Network Forecast correction for 2024: https://digitalnetwork.pl/raporty/raporty-biezace/

TIKR.com