Kneat: A Capital Light Smallcap SaaS Business You Can't Ignore - Part 2

Kneat is a software business dominating the Life Sciences validation software niche with a signficant opportunity to become the premier enterprise solution.

Kneat.com (TSE: KSI, market cap $600M CAD) is a niche software business in the Life Sciences validation space.

In Part 1 I covered the business model and competitive landscape. Readers can view Part 1 here.

Now in part 2, I examine valuation and the assumptions required to justify today’s stock price, as well as management and their capital allocation decisions. Finally, I try to answer some common questions that are likely to come up when researching Kneat.

I’ve also decided to open up paid subscriptions. I intend to publish at least 1 new investment idea that I’ve been researching for paid subs only in March (it’s a fast-growing high ROIC Polish microcap trading at around 11 times earnings that I’ve hardly seen anyone else on FinX or Substack mention, suitable for individual investors and small funds). Going forward, I intend to publish a “High Quality Business” writeup once per month (may or may not be actionable) and “Immediately Actionable Ideas” as I come across new opportunities.

Paid annual subs will start at $248 USD annually or $29 USD monthly (approximately 30% cheaper for annual). The rest of this article on Kneat will remain free, meaning there is currently no paid content. Thus, I do not blame anyone for waiting to initiate a subscription.

Management and Capital Allocation

Insider Ownership & Aligned Incentives

As of the 2024 Annual Information Form(“AIF”), Kneat's insiders own approximately 14% of the company, or 13.5 million shares. This is down from 23% of the company, or 19.8 million shares reported on the 2023 AIF. I browsed through filings on SEDI as well as CEO.ca but the reports are a bit messy to get through. It looks like the CEO and CFO have been exercising options and selling shares throughout 2024.

The management information circular discloses precise insider share ownership counts, but this doesn’t come out until late April or May. So all we have is 2024’s management information circular for now.

Two key non-executive insiders hold notable ownership stakes in the company: Ian Ainsworth, the Chairman, and Wade Dawe, a director.

Ian Ainsworth owns approximately 2% of the company, or just under 2 million shares. Wade Dawe owns a little under 7% of the company, with around 5.8 million shares. CEO Ryan Edmund and CFO Hugh Kavanagh both own around 4 million shares each, or about 4.7% of the company each.

Overall, even with insider ownership declining from 23% to 14%, I believe insiders remain highly aligned with shareholders. However, if this decline continues for a couple more years, I would reconsider.

Capital Allocation Decisions

Kneat has not had to make any external capital allocation decisions. They do not make acquisitions. Kneat has invested all its money back into the business over time, and the only capital allocation decision has been how to best spend this capital internally.

Given the revenue growth and gross margin expansion Kneat has experienced in recent quarters, it seems fair to say they’ve done well at allocating capital to the correct internal resources.

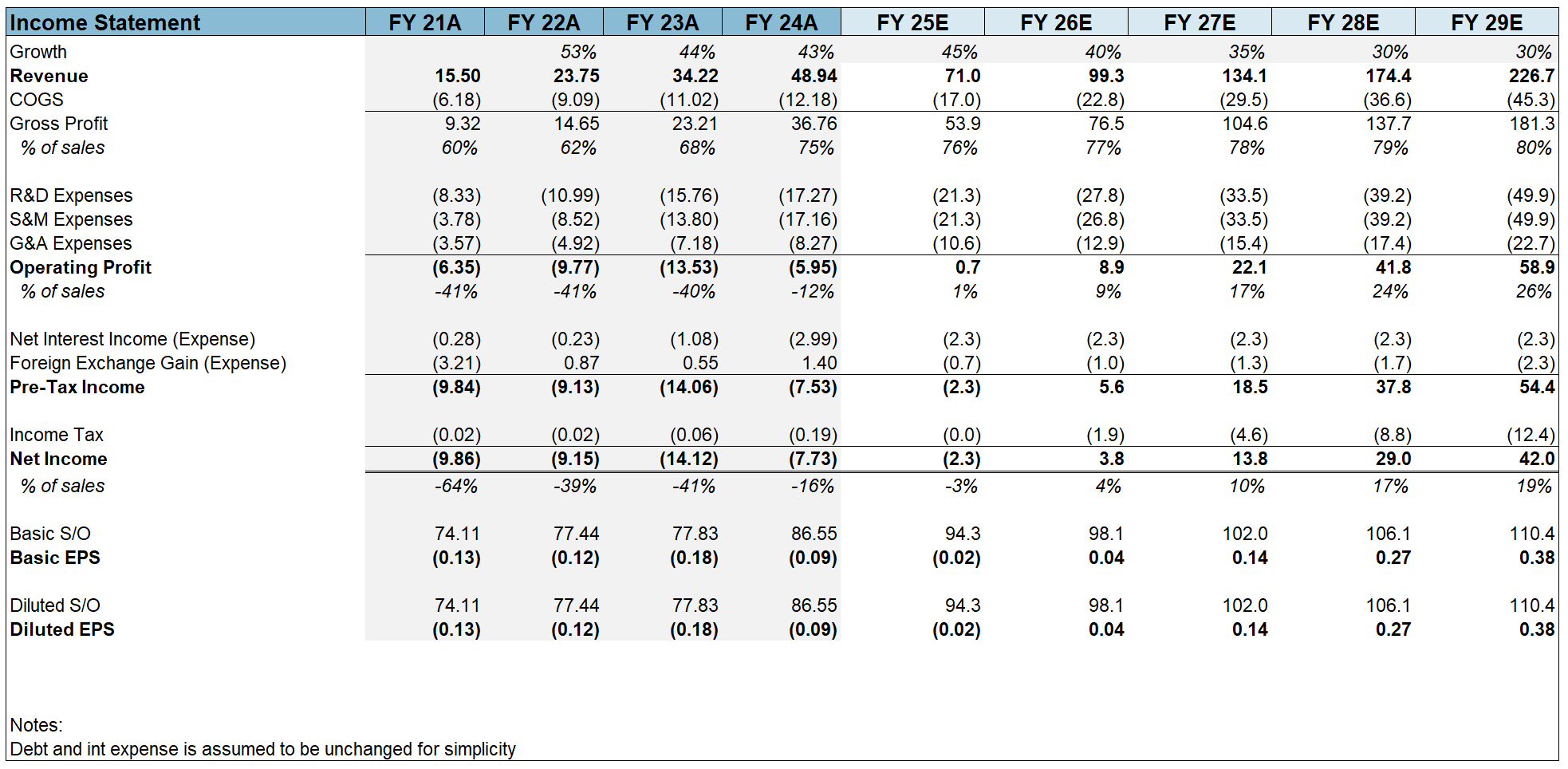

In FY2024, Kneat expensed $17M on Research & Development (worth noting here that Kneat capitalizes R&D costs), $17M on Sales & Marketing, and $8M on General & Admin expenses. The most significant increase here was in S&M. In 2021, Kneat spend just $3.8M on S&M, half of what they spent on R&D. This is a reflection of the business maturing into more than just a product. The product may be great, but the company now needs to build a salesforce to sell it.

Kneat hasn’t provided guidance around where these numbers might go going forward, which makes forecasting difficult. But internal spending likely remains Kneat’s only real capital allocation decision for the near future.

Financial Model, Valuation, and Assumptions

For now, I’m keeping my financial models relatively simple with just the income statement. I am assessing whether to make full three-statement models as well as DCF models (including a reverse DCF) available to readers in the future. Part of the delay in this Part 2 writeup going out was due to investing some time into building a full 3-statement model from scratch. After some deliberation and the realization this would take too long, I’ve decided to simplify for now and use a basic income statement, but I’ll continue to investigate 3-statement models. These models take a considerable amount of time, so I’m interested to know if this would be valuable. Such models would likely be behind the paywall due to the time investment required.

Kneat is a difficult company to forecast accurately given the company is still early in its growth phase. Will revenue growth be 30% going forward? Could they do 40%? Compounded over 5 years, that difference is substantial. At 30%, Kneat would be a $185M business by 2029. At 40%, that number would climb to $270M (nearly 50% larger). And then there’s the question of how one models expenses? As operating leverage kicks in, expenses will rapidly decline as a percentage of revenue, so simply averaging past years will not work with an early-stage rapid growth company like Kneat.

I’m projecting Kneat to grow revenue by 45% to about $71M in 2025. ARR would likely be closer to $80M in this scenario. I’ve decided to follow the industry standard for forward projections and simply reduce the revenue growth rate by 5 full percentage points per year out to 2029. My expenses as a percentage of revenue are honestly just guesses (after all, what are estimates but a series of informed guesses?) So here’s what that looks like:

Kneat finished 2024 at $59.7M of ARR adding $22.3M throughout the year, including $9.8M in Q4 alone. As I stated above, $80M of ARR by the end of 2025 no longer seems unreasonable, and in fact seems likely as Kneat’s salesforce executes. This figure actually represents less on an absolute dollar basis than what Kneat added in 2024.

Kneat has $58M of cash on the balance sheet and $23M of debt (excluding contract liabilities and lease liabilities). There are just under 94M shares outstanding as of the end of 2024.

Putting this all together with the stock price at $7.00 gives us a market cap of $657M and an enterprise value of $622M. Thus the stock trades at an EV/ARR of 10.4 on 2024’s trailing number, and an EV/ARR of 7.8 on 2025’s projected $80M of ARR. While that certainly is no small multiple, the growth rate this company has been putting up and gross margins they have would, in my opinion, justify something closer to 10X 2025 ARR by the end of the year. This would put the stock price close to $9.00, or about 30% upside.

Note: Since originally writing, the stock price has sold off to around $6.30. This selloff has been entirely systemic with the overall market, as Kneat has not reported any new news since the earnings report on February 26.

Looking out to 2029 I have the company at about $226M of revenue and $0.38 of EPS. Admittedly, these are projections that will almost certainly prove incorrect. Nonetheless, a revenue multiple of 8X in 2029 would put the company at a $1.8 market cap, or about 3 times what it is today. This would be about a 25% CAGR from the current level and put the stock close to $20. Further, this implies about a 50X earnings multiple in 2029. Very high indeed, but not unreasonable for a still-fast-growing recurring revenue software business. Of course, if growth slows beyond 2029, a 50X multiple would not be justifiable.

Ultimately, it would not surprise me if Kneat traded toward $8.50-$9.50 by the end of this year.

One thing worth noting here is that I have gross margins growing to 80% by 2029. Kneat’s COGS increased just $1.16M in 2024 over 2023, while revenue grew $14.7M, meaning Kneat produced $13.56M of incremental gross profit on $14.7 of incremental revenue, for an incremental gross profit margin of 92%! Hence, long term, gross margins may climb well above the 80% I’ve modelled.

Some Thoughts On Q4/FY24

Kneat’s Q4 was very strong, with the main point being the addition of $10M ARR in a single quarter (growing 60% YoY). Kneat’s Q4 is often seasonally strong for additions, so I do not expect that much again in any of the next 3 quarters in 2025.

On the earnings call, Kneat highlighted 4 strategic customer wins this quarter plus a partnership with Capgemini (EPA: CAP, €26B). Details were a bit light, but it appears the Kneat Gx platform now integrates with Capgemini products, offering greater value to customers that also use Capgemini. These types of partnerships illustrate Kneat’s increasing scale advantage relative to competitors. Smaller competitors are unlikely to be able to develop these partnerships. Customers get greater value due to Kneat Gx offering better integration and more use-cases. Everyone wins, except of course, Kneat’s competitors.

Questions Not Yet Answered

Why Kneat? Why hasn’t someone already digitized this? It’s 2025; surely this has been built already?

In many ways, Kneat has been the first mover here for over a decade. Kneat has been building its platform since 2007. Large Life Sciences companies are unlikely to build niche software on their own. Larger companies like Veeva have focused on larger markets with larger TAMs.

Thus, the answer is that someone has built and digitzed this - it’s Kneat! Now it’s time to scale it.

Is Software Really Capital Light?

Kneat spends almost nothing on CAPEX and has very few tangible assets on the balance sheet, allowing it to meet the traditional definition of a capital light or asset light business.

But, as I mentioned in Part 1, software businesses spend heavily through OPEX rather than CAPEX until they reach scale. Some would argue this means software is rather capital intensive.

For the purposes of this newsletter, I will consider companies with low CAPEX and low tangible assets to revenue as capital light. Thus, I’m including Kneat, and I’ll let others debate the merits of whether or not software is “capital light.”

Is This A Future High ROIC business?

It appears to me that Kneat would be a high return on invested capital business for the following reasons:

As discussed, Kneat holds little in terms of tangible assets. Kneat recently took on some debt to help fund future investments. If we assume that Kneat were able to earn enough profit to payoff its debt, and then exclude any excess cash, the invested capital portion of the ROIC equation would likely be a small percentage of revenue. If Kneat were modestly profitable (let’s say 10% net income margins, quite low for a software company and lower than what I’d expect from Kneat long term), ROIC would likely be quite high due to the small denominator in the ROIC equation. As profit margins scale due to operating leverage as a result of scale advantages, ROIC would climb.

Chart of ARR & NRR? Other data points?

Kneat discloses annual recurring revenue (“ARR”) every quarter and net revenue retention (“NRR”) annually.

NRR was 158% in 2022, 138% in 2023, and 151% in 2024. This means that the same customers spent 51% more on Kneat in 2024 than 2023. This metric highlights the success Kneat’s land and expand model is currently achieving.

As Kneat now enters a stage of growing its salesforce, I expect the company to land more new customers. New customers will not impact NRR until they lap a year later, so I would expect NRR to stay above 100% for the foreseeable future.

Thus, Kneat should continue to see strong existing customer expansion (measured by NRR) combined with increasingly common new customer wins (measured by ARR)

How can we track customer wins?

Kneat often issues news releases for new customer wins on their News Releases website page.

The most recent contract win as of the time of writing this (news release as of Feb 7, 2025) mentions that a multinational consumer food and drink producer has signed a deal with Kneat for its specialized health sciences division. These types of contracts have significant potential for Kneat to prove itself inside the health sciences division of a company that is not in the Life Sciences industry. These types of deals could expand Kneat’s addressable market beyond Life Sciences, which is something they’ve hinted at on recent earnings calls.

Artificial Intelligence risk?

Artificial Intelligence (“AI”) has been the dominant theme in markets for the last couple of years. How AI will impact businesses largely remains to be determined. There is substantial concern among software investors that AI will be able to write code and develop software much cheaper than human developers, potentially allowing AI-written software to replace current software companies. It seems far more likely to me that AI allows current software companies to develop software more efficiently for now, as running a software business is not as simple as writing some code. There are other factors to consider as well, such as liability, approvals, and many other factors. Therefore, I do not believe AI poses an immediate threat to software companies like Kneat, but investors should continue to monitor the progress of AI and its impact on various industries over time.

Tariffs Risk?

Any writeup these days would be incomplete without a discussion of U.S. tariffs. As of the time of publishing this piece, 25% Tariffs from the U.S. are now in effect on Canada and Mexico. China also received additional Tariffs, while the European Union and Great Britain seem to be next on the administration’s target list. Traditionally, tariffs have been applied only to physical goods crossing a border. However, tariffs have also not been a tool used in the digital age to the degree the current U.S. administration is now proposing. It is perhaps possible that tariffs are extended to certain types of digital goods such as software.

Kneat is an Irish-based company listed in Canada with operations in the U.S. It is possible that Kneat could face a “digital tariff” of some sort, should the U.S. decide to implement such a policy. It does not appear this will go into effect as a part of the 25% tariffs, but it is a development worth monitoring going forward.

Conclusion

Kneat is a competitively advantaged business with strong growth and a tremendously sticky product. The company is the premier enterprise solution among its peers set. The stock is not cheap on an absolute basis, but also not entirely expensive given the company’s growth profile, gross profit margins, and NRR.

On the day after Q4 earnings, I initiated a long position at $6.80 per share. I may add to this position should the stock fall further, however, I’m taking a more cautious approach in the current market environment.

Thumbnail Image: Ousa Chea